It was a quiet start with few noticing and fewer understanding the apocalypse that had been unleashed. Four Years Later, the repercussions are starting to bite into the home re-sales market.

As a GROK recap:

The NFIP Risk Rating 2.0 program is a modernized pricing methodology implemented by the Federal Emergency Management Agency (FEMA) for the National Flood Insurance Program (NFIP). Launched in phases starting October 1, 2021, and fully effective as of April 1, 2023, it represents the most significant update to NFIP premium calculations since the program began in 1968. Unlike the previous system, which relied heavily on flood zone maps and static factors like property elevation, Risk Rating 2.0 uses advanced technology, private-sector data, and catastrophe models to assess flood risk on a property-by-property basis.

The program aims to make flood insurance rates more actuarially sound, equitable, and reflective of a property’s unique flood risk. It considers multiple variables, including flood frequency, types of flooding (e.g., river overflow, storm surge, heavy rainfall), distance to water sources, and property-specific factors like elevation and replacement cost. This shift eliminates the use of flood zones for pricing, meaning premiums are no longer tied to broad geographic categories but instead tailored to individual risk profiles.

Key goals include addressing inequities in the old system, where lower-value homes often paid disproportionately high rates while higher-value homes were undercharged relative to their risk. Under Risk Rating 2.0, premiums better align with actual flood risk and home value, though statutory caps limit annual increases to 18% for most policyholders, phasing in full-risk rates over time. Discounts through the Community Rating System (CRS) remain, now applied uniformly across participating communities regardless of flood zone.

While the program enhances fairness and long-term sustainability for the NFIP, it has raised affordability concerns, particularly in high-risk areas where premiums may eventually rise significantly. FEMA emphasizes that Risk Rating 2.0 improves transparency, helping property owners understand their true flood risk and make informed decisions.

Blah, blah, blah ... what does that MEAN for MS Home Owners?

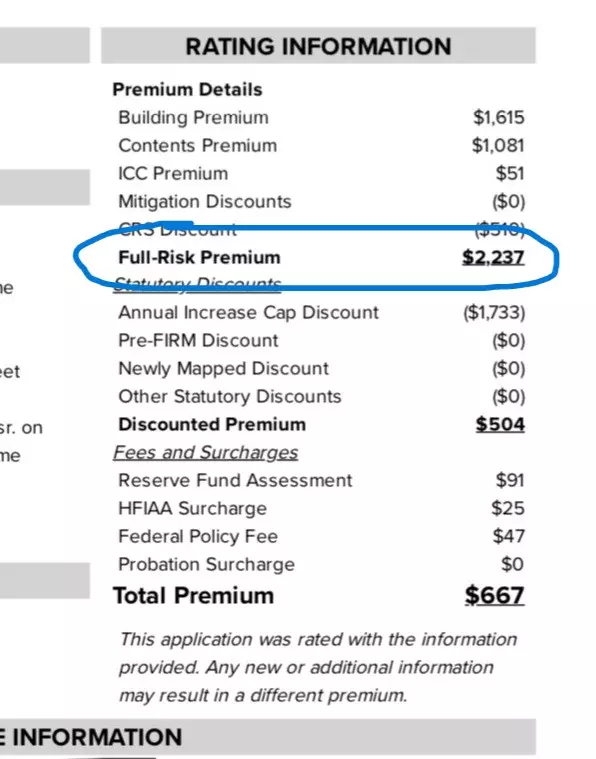

Example 1:

In Example 1, the current flood policy premium is $667/year and yet the Full Risk Premium for this policy is $2,237/year. The Annual Increase Cap Discount will decrease by 18% a year, every year until the Total Premium reaches the Full Risk Premium + Reserve Fund Assessment, HFIAA Surcharge and Federal Policy Fee.

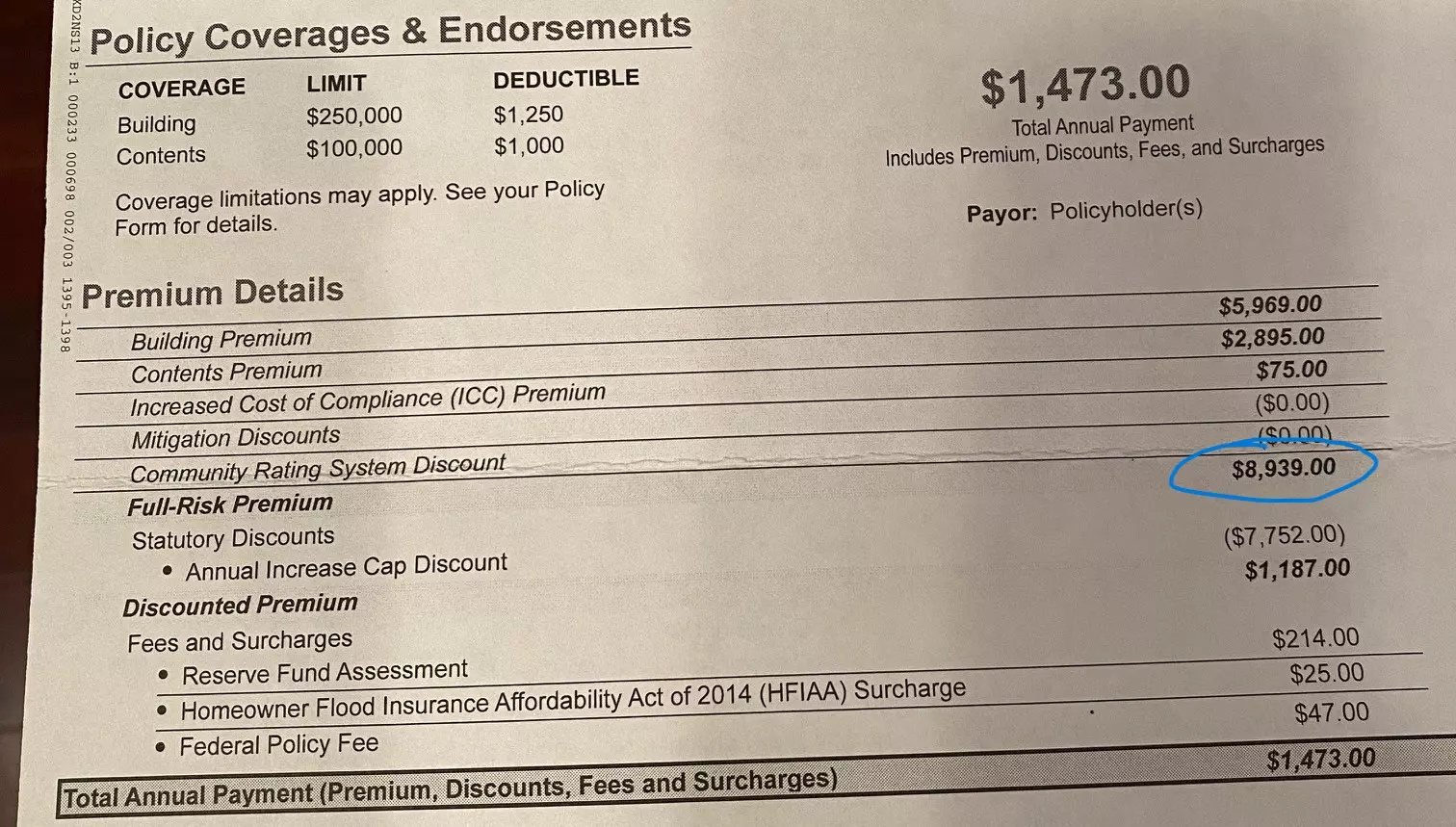

In Example 1, the current flood policy premium is $667/year and yet the Full Risk Premium for this policy is $2,237/year. The Annual Increase Cap Discount will decrease by 18% a year, every year until the Total Premium reaches the Full Risk Premium + Reserve Fund Assessment, HFIAA Surcharge and Federal Policy Fee.Example 2:

In Example 2, the current flood policy premium is $1,473/year and yet the Full Risk Premium for this policy is $8,939/year. The Annual Increase Cap Discount will decrease by 18% a year, every year until the Total Premium reaches the Full Risk Premium + Reserve Fund Assessment, HFIAA Surcharge and Federal Policy Fee.

In Example 2, the current flood policy premium is $1,473/year and yet the Full Risk Premium for this policy is $8,939/year. The Annual Increase Cap Discount will decrease by 18% a year, every year until the Total Premium reaches the Full Risk Premium + Reserve Fund Assessment, HFIAA Surcharge and Federal Policy Fee.Why does this primarily effect homes built before 2010? Current Mississippi Flood Maps were adopted in Oct 2009 following the data collected after 2005's Hurricane Katrina landfall. Homes built in 2010 are likely to meet the current elevation requirements. Homes built prior to this date,or permitted under the old elevation requirements, are likely to be below the current requirements and thus may suffer the consequences.

To make matters worse (because it can always get worse) private flood insurance companies are entering the market. On the positive side, pre-2010 homes in low flood risk areas may enjoy significant cost savings with a private flood policy. We saved a client >$1,000/year by switching him from an NFIP to a private flood policy and yet, these low risk policy holders were cross-subsidizing high risk policies.

Cross-subsidization occurs when the premiums paid by low-risk policyholders are used to offset or reduce the costs of coverage for high-risk policyholders within the same insurance pool. In this setup, the lower-risk group essentially "subsidizes" the higher-risk group, helping to keep premiums more affordable for those who face greater exposure to loss.

Supposedly, RR2.0 was to migrate away from cross-subsidization. With Private companies poaching the low-risk policies, those stuck in high risk areas should prepare for greater than predicted flood policy premiums.

If you want to:

find your ideal home,

negotiate the lowest price,

secure the best financing and

meet YOUR home buying needs with the least hassle and MOST protection...

Our VIP Home/Land Finder Service may work for you.

We would like to hear from you! If you have any questions, please do not hesitate to contact us. We are always looking forward to hearing from you! We will do our best to reply to you within 24 hours !